Property remains one of the most popular ways Canadians build wealth. As of 2024–2025, roughly 66% of the population—approximately 10 million people—live in owner-occupied homes, according to recent census data. But when a property isn’t a primary residence, it falls under a different category: real estate investment.

Property investors own nearly one in five homes in British Columbia, Nova Scotia, New Brunswick, and Ontario. With Ontario home to nearly 40% of the country’s population, the province provides a revealing lens into how investor activity impacts both rent and home prices.

The Investor Effect: Rent Growth in Mid-Sized Markets

Investors in Ontario typically own condominium apartments—not surprising, as these units are easier to rent out and often located in urban centers. According to Statistics Canada, established property investors are also more likely to own multiple properties, contributing further to investor-driven market dynamics.

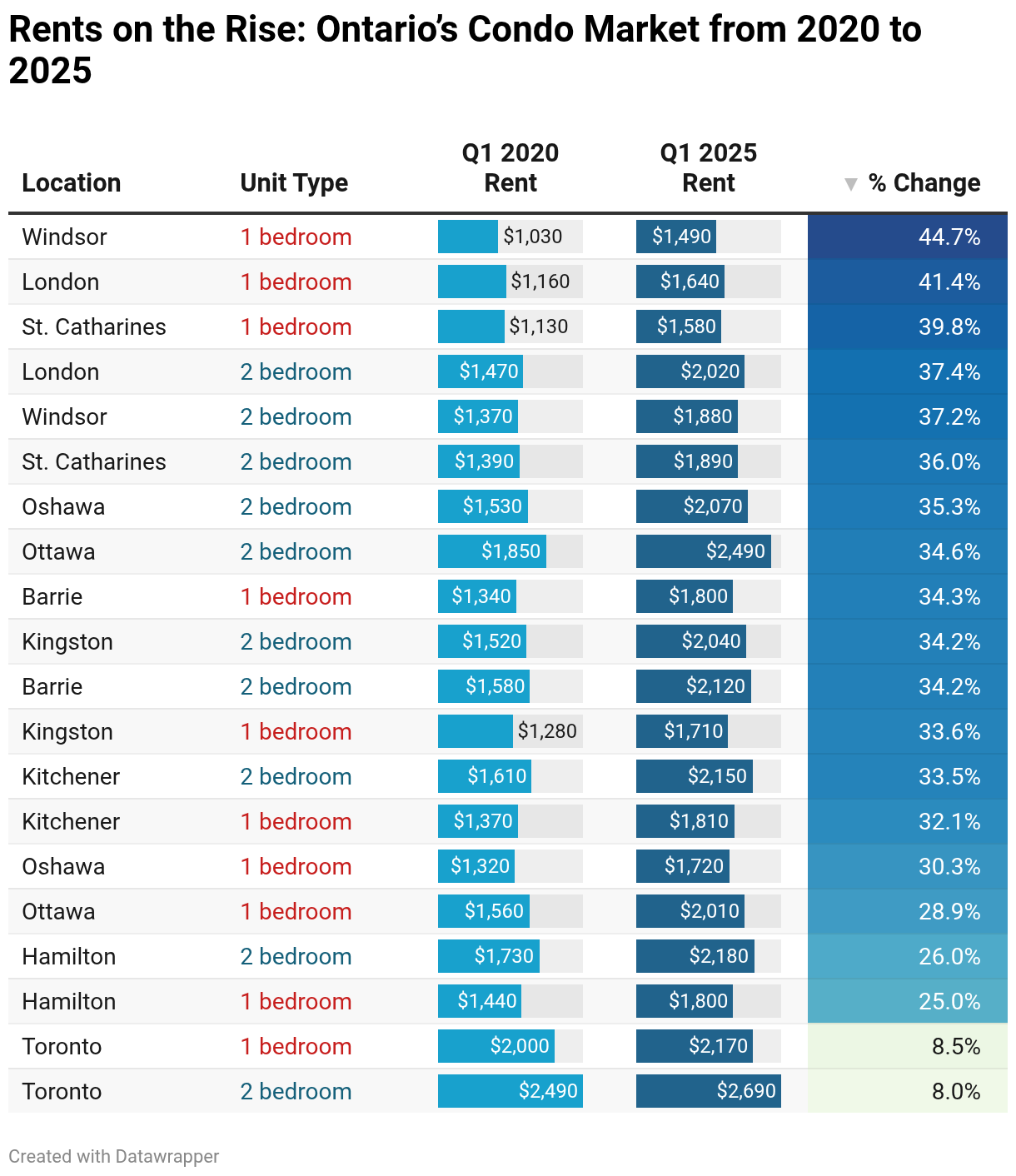

Between 2020 and 2025, rent prices across Ontario’s mid-sized cities surged, particularly in the one-and two-bedroom apartment segments that are most attractive to real estate investors.

These are the very unit types typically purchased as income properties, and in cities where investors owned a high proportion of condos, the rent increases were consistently more dramatic. The trend is clear: in markets where over 50% of condominiums were investor-owned, one- and two-bedroom rents rose between 32% and 45% over five years.

Windsor exemplifies this trend. With 64.4% of condos investor-owned, it recorded the highest one-bedroom rent increase in the province at 44.7%, while two-bedroom rents climbed 37.2%. Notably, this occurred despite relatively modest growth in Windsor’s home sale prices, reinforcing the idea that rent inflation was driven more by investor competition and constrained rental supply than resale activity.

Similarly, London, where 85.5% of condos were used as investment properties (the highest investor share in Ontario), saw one-bedroom rents rise 41.4% and two-bedroom rents increase 37.4%, positioning it as another high-impact city for investor-driven rent growth.

In Kitchener-Waterloo, where investors owned 60.7% of condos, rents rose 32.1% for one-bedrooms and 33.5% for two-bedrooms, signaling that high investor presence places consistent upward pressure on rents even in cities with more balanced housing demand. Kingston and St. Catharines also support this trend.

Kingston, with 46.5% investor condo ownership, experienced a 33.6% increase in one-bedroom rents and 34.2% in two-bedrooms. In St. Catharines, where investors owned 54.7% of condos, one-bedroom rents jumped 39.8%, while two-bedrooms rose 36%. These markets share similar conditions: high investor participation, strong demand for rental units, and relatively limited new rental construction—all of which combine to push rents upward.

Even in cities with slightly lower investor ownership, like Barrie (36.1%), rent increases remained significant, with one-bedroom rents up 34.3% and two-bedrooms 34.2%. These figures suggest that while investor ownership isn’t the only factor at play, it acts as a force multiplier when layered onto local population growth and supply constraints.

In contrast, Toronto, despite having a large investor presence in its condo market, saw the most subdued rent increases: just 8.5% for one-bedrooms and 8% for two-bedrooms between 2020 and 2025. This anomaly is likely explained by Toronto’s larger supply of purpose-built rentals, greater regulatory oversight, and unique COVID-related impacts on the downtown rental market. While investors are still active in Toronto, their influence is diluted across a much larger housing ecosystem.

Overall, the data paints a compelling picture: rent inflation in Ontario’s mid-sized cities has been closely tied to investor activity in the condo market. Where investors own a significant share of available apartments, rental supply tightens, competition increases, and rents rise at a much faster rate—particularly for one- and two-bedroom units. These conditions create persistent affordability challenges for renters, especially in cities that already lack diverse, purpose-built rental housing options.

When Rents Rise, So Do Prices, But Not Always Equally

Meanwhile, a closer look at Ontario’s housing data between 2020 and 2025 reveals a compelling and increasingly consequential pattern: cities with the highest share of investor-owned condominiums didn’t just see rent and apartment prices climb. Ultimately, these cities also experienced some of the strongest single-family home price growth, suggesting that investor activity may be reshaping the entire local housing ecosystem, not just the condo segment.

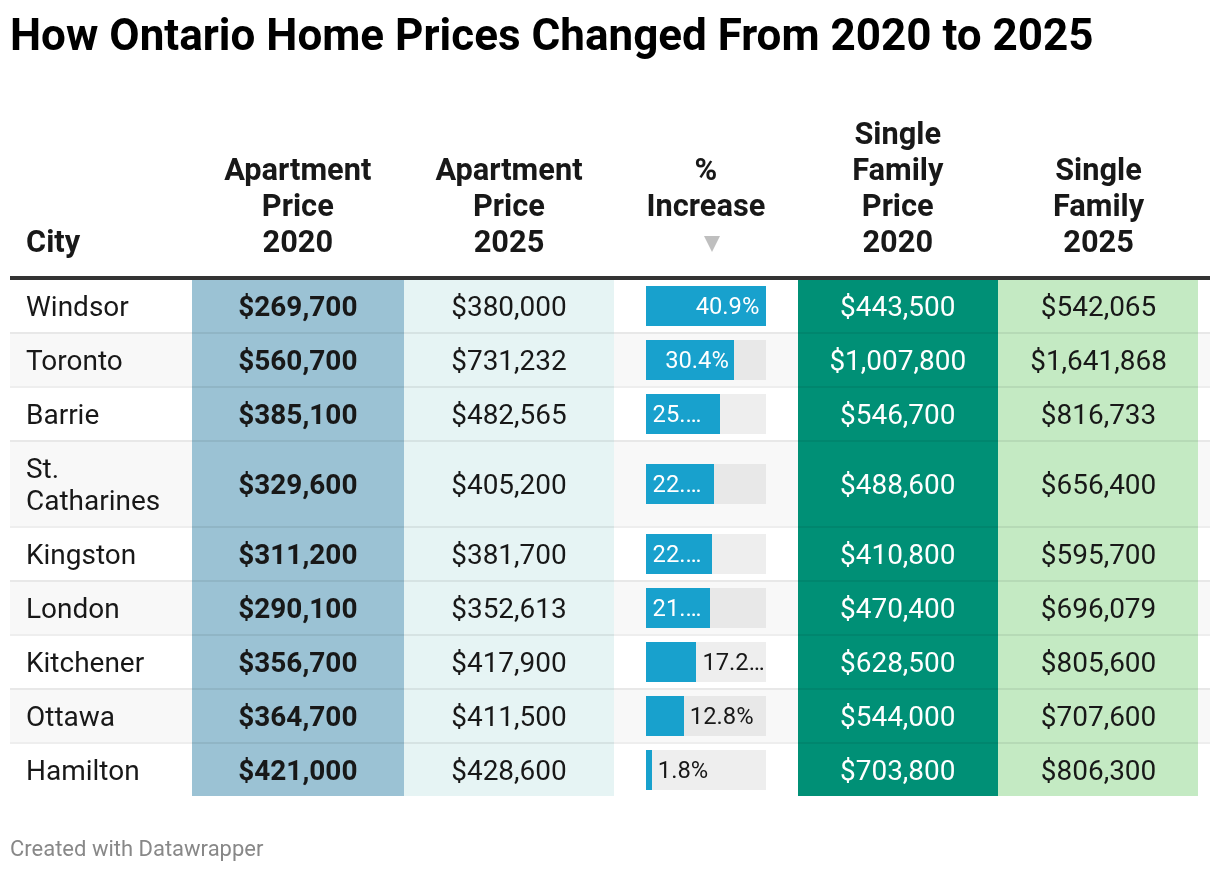

Consider London, where a staggering 85.5% of condos were owned by investors. Over five years, apartment prices rose by 21.5%, but detached home prices soared by 48%. While investors may have primarily targeted condos, the ripple effect likely spilled into the single-family market. Investors bidding up prices for smaller, more affordable housing units, paired with the city’s rapid population growth, may have indirectly nudged first-time buyers and families into competing for detached homes, amplifying demand and pushing prices higher across the board.

Windsor offers another striking case. The city had the highest apartment price increase (40.9%) among all Ontario cities, despite having one of the lowest single-family home gains at 22.2%. This sharp imbalance suggests that in markets where single-family homes are still relatively affordable, investors are laser-focused on condos for rental income, driving disproportionate price growth in that segment while keeping detached housing somewhat insulated—at least for now.

Meanwhile, Kitchener-Waterloo saw below-average price growth in both housing types: apartments up 17.2%, and single-family homes rising 28.2%. This indicates a market where investor and end-user demand coexist, with both contributing to overall housing inflation.

In St. Catharines, apartment prices rose 22.9% while detached homes jumped 34.3%, reinforcing the idea that investor-heavy cities are not just hotbeds for rising rents, but catalysts for broader price pressure in the ownership market.

The most surprising correlation emerges when looking at Barrie, a city with relatively moderate investor condo ownership at 36.1%, yet it experienced one of the highest single-family home price increases (49.4%) and a 25.3% gain in apartments. This suggests that even with modest investor activity, cities perceived as “affordable alternatives” to the GTA are being swept up in province-wide affordability migration, potentially drawing investor and end-user demand alike. This may signal that Barrie is in the early stages of a new growth cycle, where investor activity increases alongside population growth.

Contrast that with Hamilton and Ottawa, where investor ownership hovered around 40%, and price growth was notably weaker. While these markets have more investor activity than Barrie, they may have already peaked earlier in the market cycle and are now entering a cooling phase. Hamilton’s apartment values rose just 1.8%, and single-family prices climbed only 14.6%, reflecting a post-pandemic cooling. Ottawa performed better, with 12.8% apartment growth and 30.1% in detached homes, but still lagged behind investor-saturated markets like London and Windsor.

Investor Ownership Reshapes Affordability

From rent hikes to rising home values, the data makes one thing clear: investor activity has a measurable impact on Ontario’s housing markets. The effects are most pronounced in mid-sized cities where condo ownership is concentrated among investors and rental supply is limited.

In these markets, the competition among investors, combined with rising demand from renters, drives up costs across the board. Renters face higher monthly payments, while aspiring homeowners must contend with rapidly appreciating property prices. The result? Increased pressure on housing affordability in precisely the segments of the market where it’s needed most.