The holidays are the most wonderful (and wallet-draining) time of the year. Between gifts, travel, festive dinners, and parties, Canadians are preparing to spend big once again. According to PwC Canada’s 2025 Canadian Holiday Outlook, the average Canadian plans to spend $1,675 this season on gifts, travel, and entertainment. In some regions, that number climbs even higher, $1,821 in British Columbia and $1,788 in Ontario, while Albertans and Quebecers are a touch thriftier at $1,532.

But what if, instead of splurging on matching pajamas, Secret Santa exchanges, and plane tickets to see family, you decided to stash that holiday cash in a savings account? Could a few years of skipping the season of spending actually get you closer to buying a home? Zoocasa analyzed how redirecting this annual holiday budget toward savings could contribute to a 20% down payment in Canada’s housing market.

Spoiler alert: even if you’re on Santa’s “nice” list, the math says you’ll need more than a few quiet Decembers to afford a down payment in today’s market.

Turning Holiday Cheer Into Home Equity

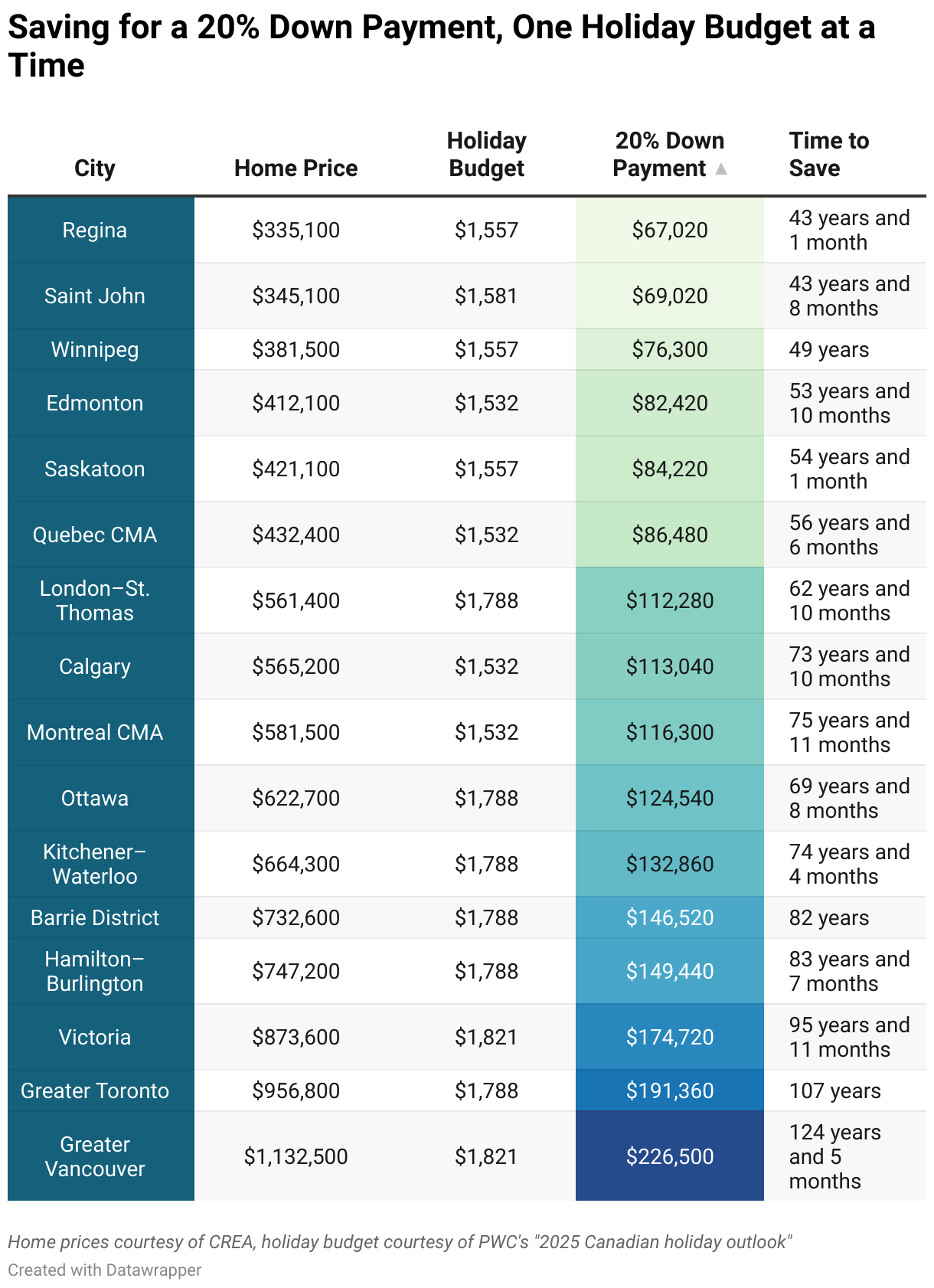

Let’s start with Edmonton, one of the country’s more affordable major markets. With an average home price of $412,100, a 20% down payment comes to $82,420. Redirecting the average Alberta holiday budget of $1,532 each year would take a jaw-dropping 53 years and 10 months to hit that goal. That’s more than half a century of saying no to holiday sales, no gingerbread lattes, and no festive family flights, all for a starter home you’d finally buy sometime around 2079.

It doesn’t get any easier out west. In Greater Vancouver, where the average home price has reached $1,132,500, a 20% down payment of $226,500 would require saving for 124 years and 5 months. You’d have to skip every holiday season from now until the year 2149 to buy your dream condo. Even Santa might retire before then.

Victoria isn’t far behind, with home prices averaging $873,600 and a savings timeline of nearly 96 years. That’s a lifetime of resisting festive markets, skipping seaside getaways, and re-gifting the same candle year after year.

The Math Feels Slightly Merrier in the Prairies

Prairie provinces offer a little more cheer, but not enough to make the Grinch start house-hunting. In Regina, where homes average $335,100, a 20% down payment of $67,020 would take 43 years and 1 month to save if you tucked away your $1,557 holiday budget each year. Saint John lands in a similar range at 43 years and 8 months for a $69,020 down payment.

Winnipeg isn’t much better. With home prices averaging $381,500, saving $76,300 at $1,557 a year would take 49 years. You’d need to skip holiday spending for half a century, enough time for your holiday sweaters to go out of style and come back again.

Even in Saskatoon, where homes average $421,100, a 20% down payment of $84,220 would require 54 years of skipped celebrations.

A Lifetime (or Two) of Skipped Holidays

Ontario homeowners might want to brace themselves. With prices climbing across the province, holiday budgets don’t stand a chance.

In Kitchener–Waterloo, where homes cost around $664,300, a 20% down payment of $132,860 would take 74 years and 4 months of saving your $1,788 holiday budget. Hamilton–Burlington and Barrie tell a similar story, clocking in at 82–83 years to save enough for a 20% down payment of roughly $146,000 to $149,000.

Even London–St. Thomas, one of Ontario’s more budget-friendly regions, would take nearly 63 years to reach a $112,280 down payment goal.

And then there’s Greater Toronto, where the average home price sits at $956,800—meaning you’d need $191,360. Saving the $1,788 holiday budget each year would take 107 years to save enough money for a down payment. You could skip every holiday from now until your great-great-grandchildren are celebrating, and still be short a few thousand.

Why Holiday Sacrifices Won’t Buy You a Home

Quebecers might enjoy more affordable housing, but even here, skipping holiday cheer isn’t enough to fast-track homeownership.

In the Montreal CMA, where homes average $581,500, saving $116,300 for a down payment at $1,532 per year would take 75 years and 11 months. Quebec City fares slightly better at 56 years and 6 months for an $86,480 down payment, but that’s still decades of re-gifting maple cookies and canceling cozy chalet getaways.Across the East Coast, holiday savings would stretch further, but not enough to make buying realistic anytime soon. In Saint John, it would take 43 years and 8 months to save a 20% down payment of $69,020. Even in Canada’s most affordable markets, skipping a few years of holiday spending simply doesn’t add up to homeownership magic.

A Reality Check Wrapped in a Bow

Across all regions, the data is clear: redirecting your holiday budget toward a down payment is more symbolic than strategic. Even in the most affordable cities, it would take four to five decades of skipping gift exchanges and family dinners to reach your goal. In high-priced regions like Toronto and Vancouver, the savings timeline stretches past a century.

That’s not to say cutting back is meaningless; building consistent savings habits can make a real difference when paired with larger financial strategies, such as downsizing, reducing car costs, or exploring more affordable regions. But the idea that you can “skip the holidays to save for a house” is as unrealistic as finding a move-in-ready detached home in Vancouver for under $500,000.

Until affordability improves, maybe the best gift you can give yourself is a little financial balance and permission to enjoy the season guilt-free. Because when homes cost hundreds of thousands more than your lifetime of holiday budgets combined, one more gingerbread latte probably isn’t the dealbreaker.